Need payment processing?

Let your Agent/ISO business take flight with CoPilot.

Our merchant management portal, made just for you. You’re busy running a business - make it easier with faster onboarding, merchant data reporting, simple device ordering and management, and more!

Track Merchant Onboarding Statuses

Track activity from application to approval, and quickly onboard new accounts with an easy-to-use digital application.

Manage Your Portfolio

Get line-item detail residual reporting and calculations, plus insights to sub-partner performance.

Get Human Support

Manage account reconciliation, submit requests via tickets and view merchants' deposits, batch reports, transactions, and more.

Connect your merchants to better technology and solutions.

Access an unparalleled product suite that puts you in the game to sell to almost any merchant, including: small shops, online retailers, restaurants, and more.

![]()

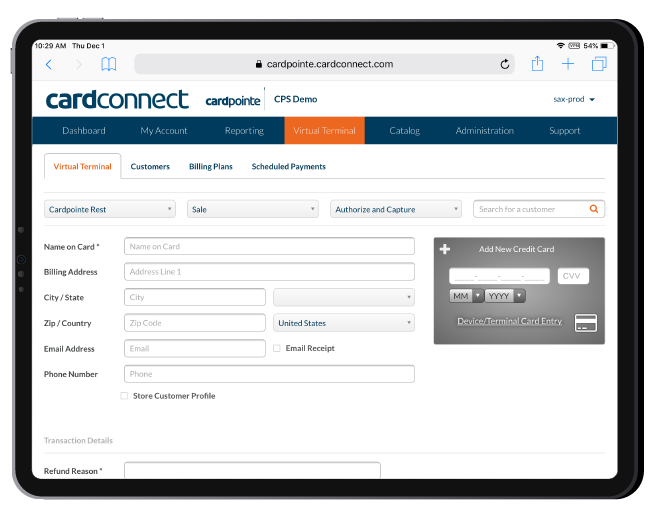

The comprehensive credit card processing platform for your merchants.

- Accept payments in-person, online, or on-the-go

- Manage transactions from anywhere

- Get the lowest processing rates with interchange optimization

- Integrate with existing platforms easily

![]()

- Customize a POS perfect for your merchants' unique payments environment

- Leverage a library of 300+ apps for tailored business needs

- Choose from a suite of flexible hardware options

Plus, gain access to our exclusive Clover and CoPilot Integration to more easily manage the Clover merchant accounts you service!

Gain an edge in selling payments.

Back your book with differentiators and leverage offerings that are built to help you win new business.

Referral incentives & rewards

Onboarding specialists to activate your success

Expert marketing & sales resources tailored to your portfolio

Direct communication with underwriting team

Access to sell the Clover product suite

Interactive webinars to keep you in-the-know

The CardConnect Difference

Don't just take it from us - find out what our partners are saying.

Contact Us

Your success in payments starts here! Please select your partnership type below so we can connect.