CardPointe payment management software.

The CardPointe platform enables businesses to easily review their credit card transactions in real-time, all from one location.

Plus, bring these features right to your fingertips with the mobile credit card processing application for Apple and Android devices.

Transaction management made simple.

Easily identify best-selling products, most loyal customers, top-performing employees, and more.

Monthly volume reports allow

users to closely monitor business performance and progress.

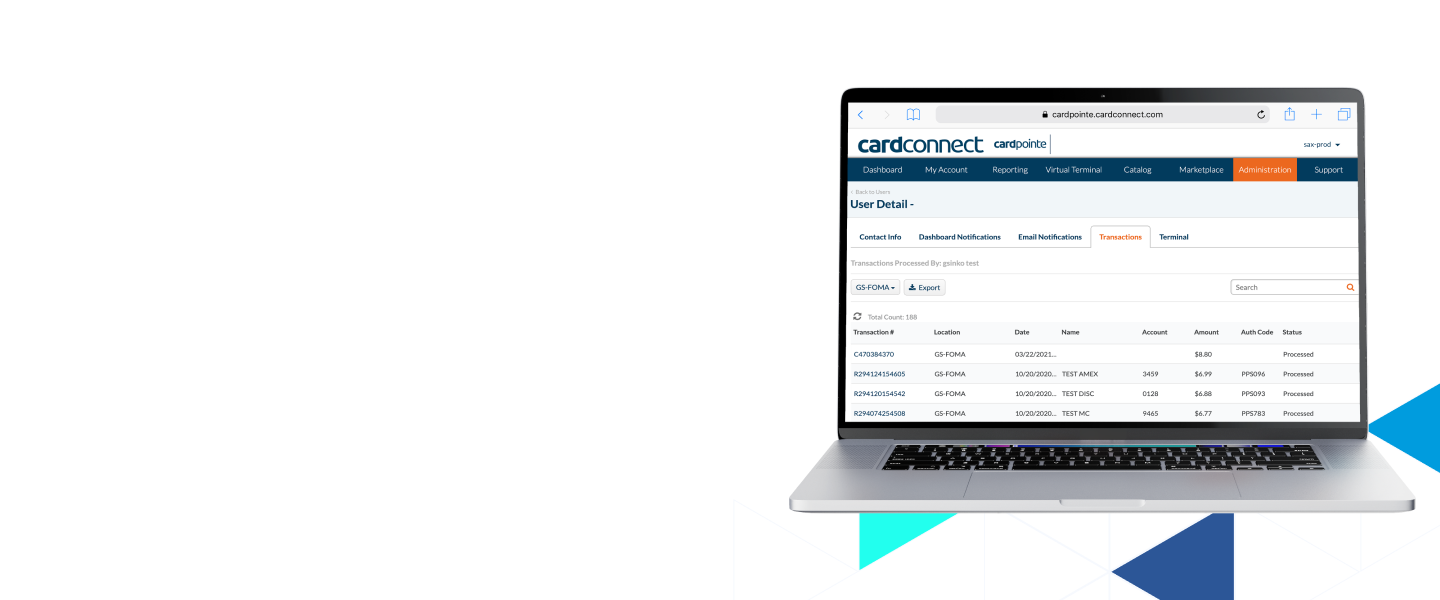

Powerful filters allow users to refine transactions using a number of parameters including date, credit card number, status, and more.

Easily access and download

reports to compare sales figures

for different locations.

Manage transactions from start to finish.

Account User Management

Manage employee user access settings at any time

Recurring Billing

Set up custom billing plans with recurring payments

PCI Compliance Management

Check compliance status at any time and use tools like the Self Assessment Questionnaire (SAQ)

Download Reports

Export point-of-sale analytics to facilitate strategic planning within a team

View Payment Trends

See how customers are paying, whether they use tap, dip, swipe, or mobile payments

Mobile App

Take business on-the-go with the CardPointe App for Android and iOS

Contact Us

Your success in payments starts here! Please select your partnership type below so we can connect.