Simple payment gateway

API integration.

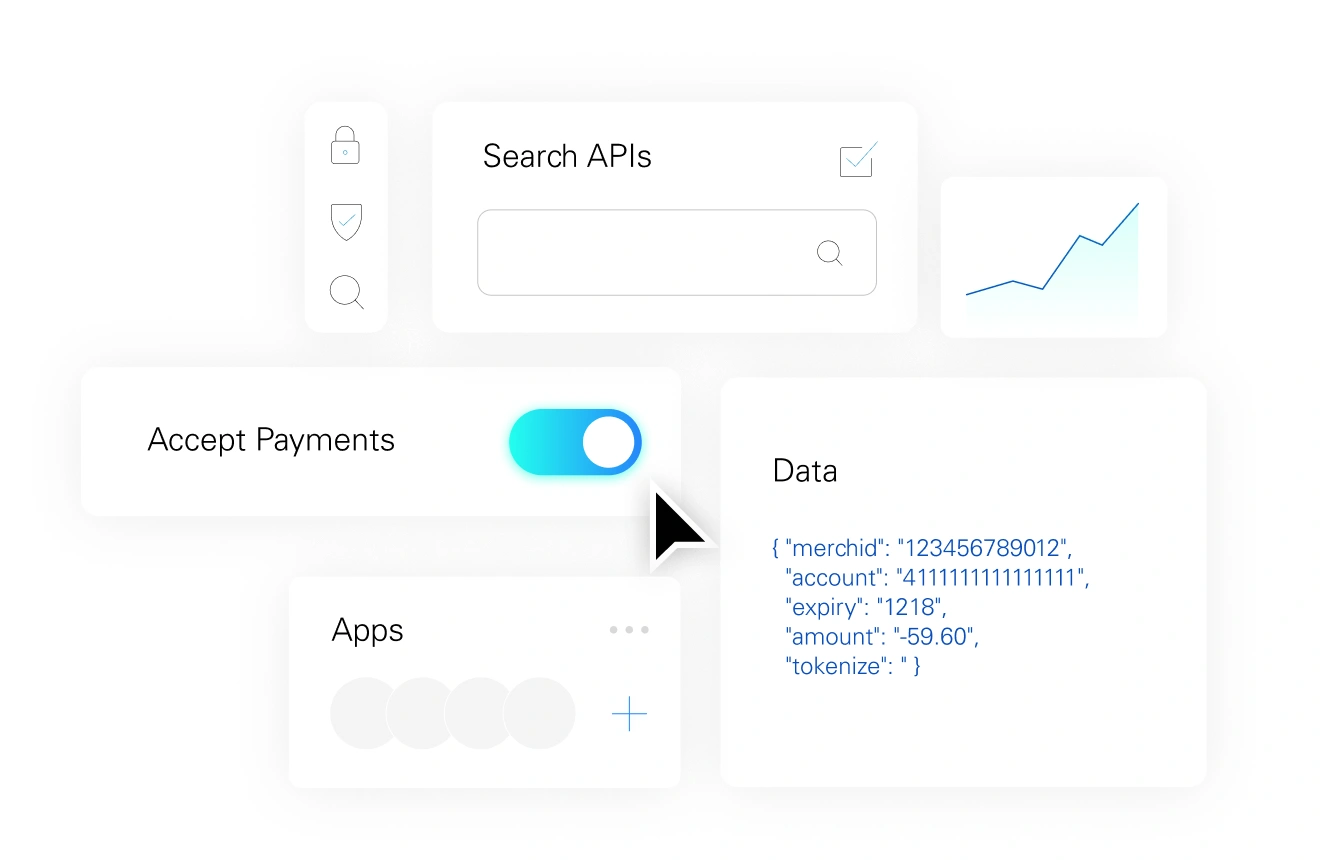

Gain access to a library of developer-friendly APIs that make it easy to accept payments through multiple channels – whether that is in-store through a POS system, or online using a checkout page or mobile app.

A perfect match for:

eCommerce Websites

Mobile Apps

Software/SaaS

ERP Systems

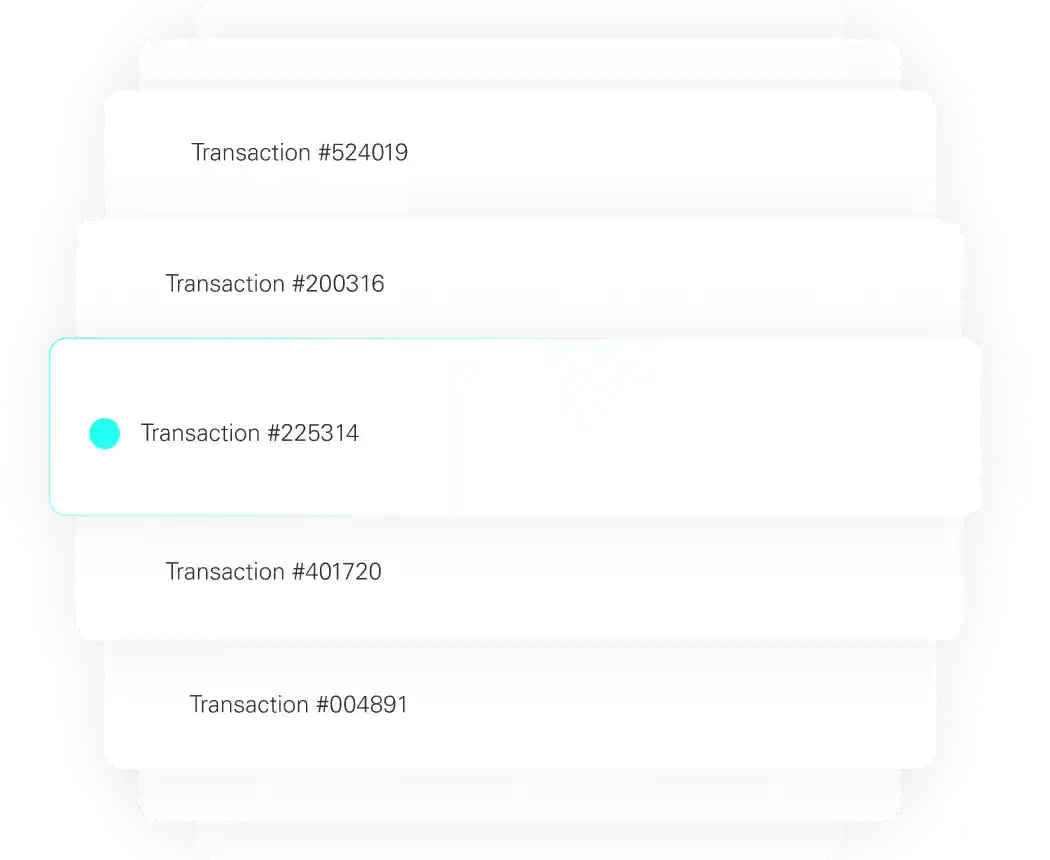

Get access to detailed

transaction reporting.

- Access to vital business data like settlements, deposits, and statements

- Comprehensive transaction reporting and functions including voids and returns

- Learn more about CardPointe transaction reporting

- Maximize Security

- Automate Recurring Payments

- Improve Customer Billing

Maximize security to minimize PCI scope.

- Protection for every transaction with CardSecure patented tokenization

- Reduced audit scope of the PCI Security Standards Council for stress-free compliance management

Got questions? We got answers.

Contact Us

Your success in payments starts here! Please select your partnership type below so we can connect.