“CardConnect has been a great partner. They deliver world-class payment technology and we can count on them to support our merchants.”

Kevin Zhao,

ZBS Solutions

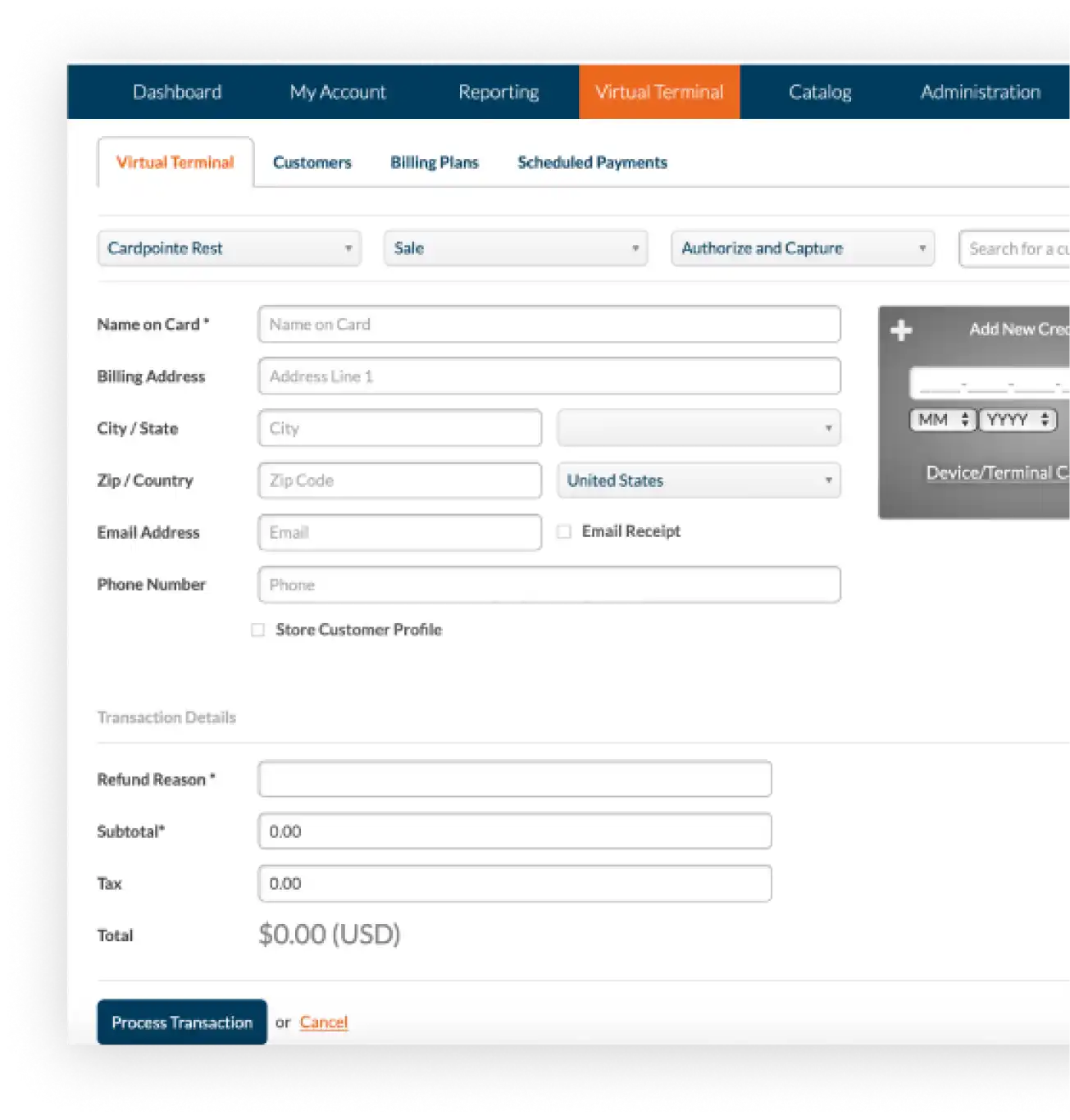

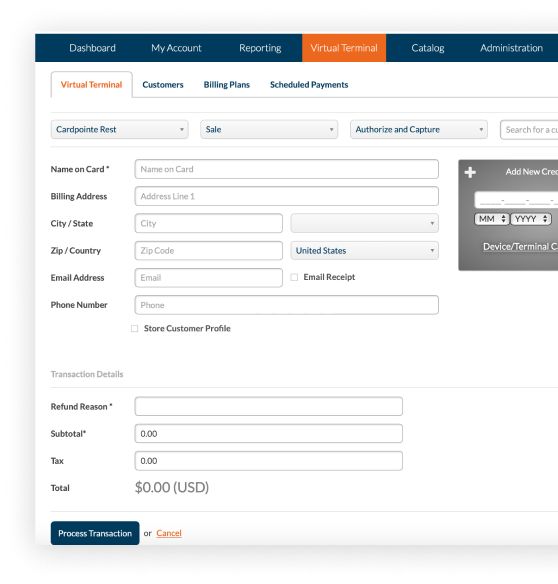

Our merchant processing solution empowers businesses with a user-friendly portal that creates a seamless experience from 'process' to 'paid'.

This comprehensive credit card processing platform also features numerous integrations and add-ons that boost its functionality and allows users to offer even greater convenience to customers.

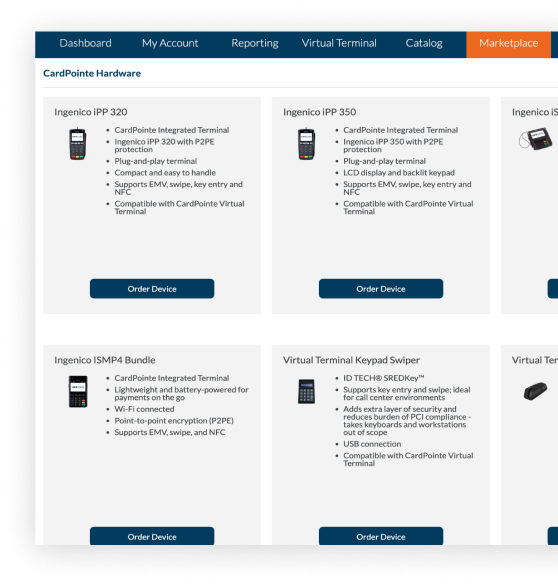

The CardPointe platform and devices include additional features that make accepting and managing payments as effortless as possible.

Plug-and-play terminal for swipe, dip, and tap transactions protected by point-to-point encryption (P2PE)

Your success in payments starts here! Please select your partnership type below so we can connect.